Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

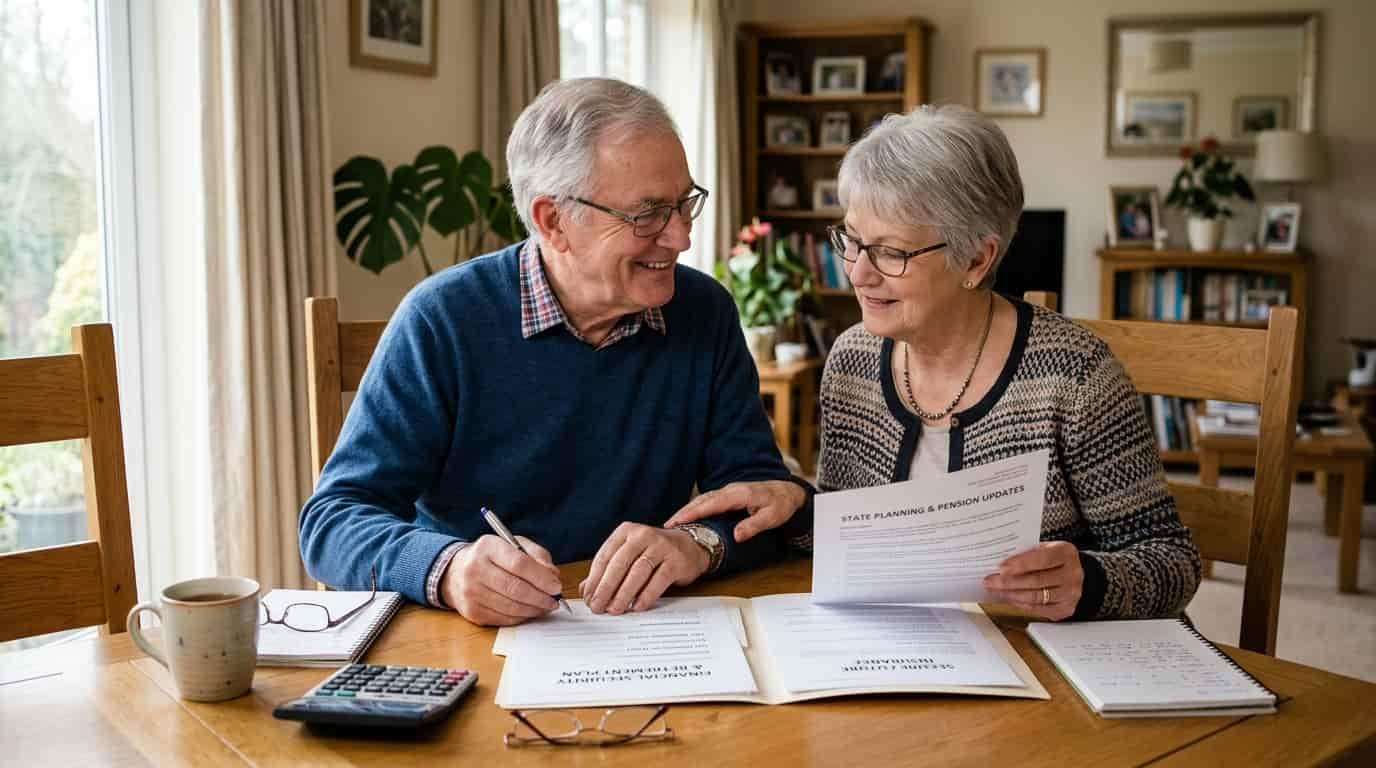

Reaching the age of 60 is often seen as a milestone of stability. Many people are retired or close to retirement, children are financially independent, and major debts like mortgages may be reduced or fully paid off. At this stage, some assume life insurance is no longer necessary.

However, life insurance over 60 remains one of the most important financial planning tools. It is not just about covering death costs—it is about protecting your spouse, maintaining financial stability, covering medical bills, and leaving a legacy for loved ones.

Whether you are 60, 65, 70, or even older, the right policy can still make a meaningful difference.

Life insurance for seniors over 60 is a financial product designed to provide a payout (death benefit) to your beneficiaries when you pass away. In exchange, you pay monthly or yearly premiums.

At this age, policies are often tailored to:

Unlike younger-age policies, life insurance over 60 focuses more on financial protection and legacy planning, not income replacement.

Many people underestimate future expenses. Here are key reasons why seniors still need coverage:

Funerals can cost between $7,000 and $15,000 or more depending on location and arrangements. Without insurance, families may struggle to cover these sudden expenses.

Even after retirement, many people still have:

Life insurance ensures these debts do not pass to family members.

If your spouse depends on your pension or retirement income, your passing could reduce their financial stability. A life insurance payout helps maintain their lifestyle.

Many people over 60 want to leave money for:

Life insurance is a simple way to transfer wealth.

While not directly covering medical bills, insurance can help families manage costs associated with long-term care or final medical expenses.

Understanding your options is critical. Not all policies are the same.

Term life insurance provides coverage for a specific period (10, 15, or 20 years).

Pros:

Cons:

Best for: Seniors who want affordable, temporary protection.

Whole life insurance provides lifelong coverage and builds cash value.

Pros:

Cons:

Best for: Long-term planning and wealth transfer.

This is one of the most popular options for people over 60.

Pros:

Cons:

Best for: Covering funeral and small debts.

No health questions, no medical exam.

Pros:

Cons:

Best for: Seniors with health issues who still need coverage.

This depends on your financial situation.

Here’s a simple breakdown:

A good rule: choose enough to avoid financial burden on your family.

Premiums increase with age, but policies are still accessible.

Factors affecting price:

Smokers and individuals with chronic illnesses pay more.

Yes. Many insurers offer policies even with conditions such as:

Options include:

However, premiums will be higher and coverage may be limited.

No-exam policies are extremely popular among seniors.

This is ideal for seniors who want convenience and quick approval.

Many seniors make costly mistakes when buying life insurance:

The older you get, the more expensive coverage becomes.

$5,000 may not be enough even for basic funeral costs.

Some policies have waiting periods or exclusions.

Prices vary significantly between companies.

Some people overpay for coverage they don’t need.

Follow these steps:

Ask:

Choose monthly payments you can comfortably afford.

Term vs whole life vs final expense.

Medical exam or no medical exam?

Look at:

Most financial experts recommend:

A combination strategy is also common.

Yes—absolutely, depending on your goals.

It is especially valuable if you:

Even small policies can make a big difference.

Life insurance over 60 is not about fear—it is about responsibility and planning. Whether your goal is to cover funeral expenses, support your spouse, or leave a financial gift, there are flexible options available for every budget and health condition.

The key is to choose early, compare carefully, and select a policy that matches your real needs—not just marketing promises.

With the right plan, you can ensure peace of mind for yourself and financial security for your loved ones.